Top Headlines – Key Global Developments

- Bitcoin extends sharp losses as broader crypto markets remain under pressure and risk sentiment weakens globally

- Asian equity futures mixed after US data delays spark volatility and uncertainty over underlying economic momentum

- Oil rises as OPEC+ maintains output strategy and supply concerns persist after infrastructure strikes

- UK political pressure intensifies following the OBR leak and continued scrutiny of Reeves’s fiscal framework

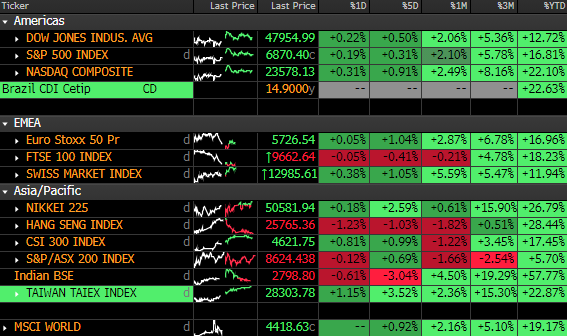

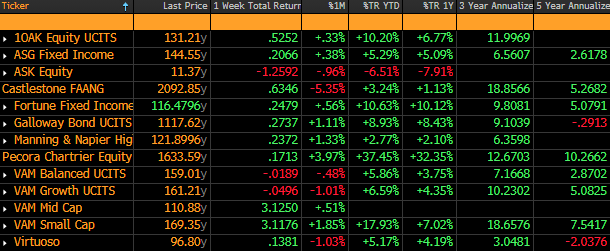

Markets Snapshot – Monthly and YTD Performance

United States – What’s Moving Markets

- Market volatility intensified last week following delayed US data releases and a stronger-than-expected payroll figure that briefly lifted equity futures

- Nvidia’s upbeat earnings supported early risk appetite before concerns around rising unemployment pulled major indices lower

- Treasury yields moved sharply as FOMC members delivered mixed signals on the likelihood of a December rate cut

- Sentiment is being shaped by conflicting macro signals — stronger payrolls data, rising unemployment, delayed releases clouding visibility, and divergent Fed communication — leading investors to hedge tactically across equities, volatility products, and front-end rates

Middle East – Market Sensitivities and Geopolitical Risks

- Oil markets remained supported by supply-side risks following Ukrainian strikes on Russian energy infrastructure

- OPEC+ reaffirmed its output stance, helping stabilize crude after recent volatility

- Regional sentiment is being influenced by supply disruptions, OPEC+ policy stability, and heightened geopolitical tensions, which together are contributing to firming crude prices and cautious positioning in regional energy-linked assets

Europe – Key Drivers and Sentiment Shifts

- Eurozone sentiment remains fragile as disinflation progresses, with CPI edging further toward target

- German industrial indicators show uneven momentum, reinforcing concerns about deeper structural slowdown

- Political focus remains elevated as the UK continues dealing with the fallout from the OBR’s early publication and fiscal-credibility concerns

- Regional sentiment is being driven by steady but slow euro-area disinflation, weak industrial data out of Germany, and persistent scrutiny over UK fiscal governance following the budget-report leak, all of which are shaping a defensive tone across European risk assets

SailWealth Fund Performance

Asia-Pacific – Trade Momentum and Strategic Shifts

- Asian markets mixed as investors weigh US-data-related volatility alongside ongoing concerns about economic momentum in China

- Manufacturing indicators across the region continue to show patchy recovery, with trade-exposed economies feeling the slowdown in US and EU demand

- Equity flows remain selective, with investors favouring markets showing policy support or currency stability

- Sentiment is being shaped by uneven regional growth, uncertainty stemming from US macro signals, and cautious rotation into markets with clearer policy direction, keeping Asia-Pacific risk-taking fragmented

South America – Trade Positioning and Political Realignment

- Argentina continues to experience FX instability as the peso faces renewed downward pressure

- Sovereign funding conditions remain challenging across the region despite firmer commodity backdrops

- Sentiment is being driven by currency volatility, tighter external financing conditions, and investor caution surrounding political uncertainty, limiting broad-based participation in South American assets

Australia – Steady Gains Amid Global Sensitivity

- Australian equities remain supported by financials and select resource names

- AUD trades defensively amid global risk-off tone and uncertainty around US data

- Sentiment is being shaped by resilient domestic equity drivers, a softer Australian dollar responding to global volatility, and investor preference for defensive sector exposure while monitoring external macro risks

Global Equity Volatility Has Spiked

Equity volatility surged to multi-month highs as delayed US data and mixed macro signals triggered sharp swings across equity markets

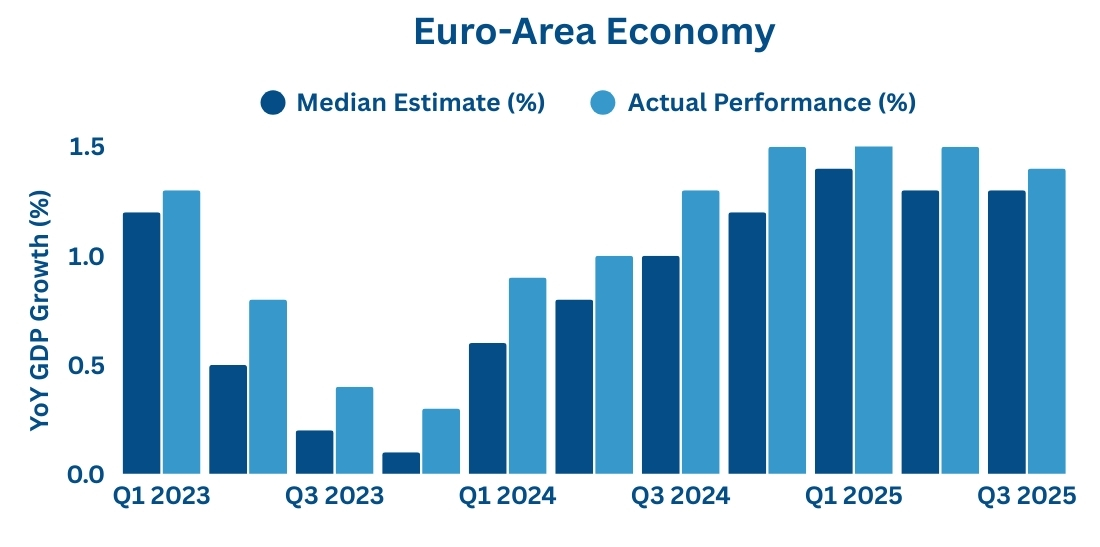

China GDPEuro-Area Economy Is Outperforming ExpectationsGrowth

Euro-area growth continues to beat expectations as services resilience and easing supply constraints support activity

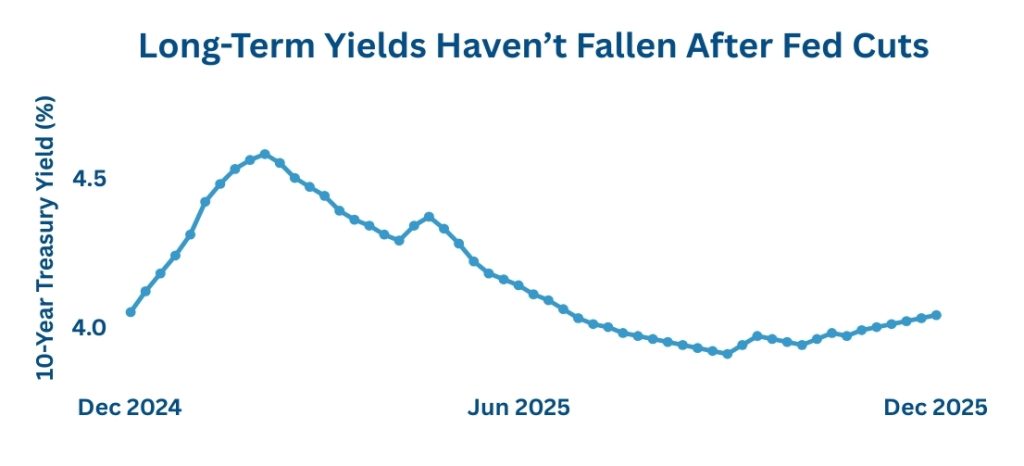

10-year Treasury yields remain elevated despite policy easing

Long-term yields remain sticky as term premium rises and markets reassess the durability of US inflation